The labor market is primed for a soft landing

Current labor market strength rests on fundamentals that look... normal

A great deal of recent debate has focused on whether steps taken by the Federal Reserve to reduce inflation will also weaken the labor market and cause a recession. Many indicators currently suggest that the labor market remained very strong by recent historical standards over the last three months, though some have weakened relative to the preceding three months. Looking ahead, labor market performance comparable to 2019 seems sustainable, creating a real opportunity for a so-called soft landing if the recent moderation in inflation continues.

The labor market is currently quite strong

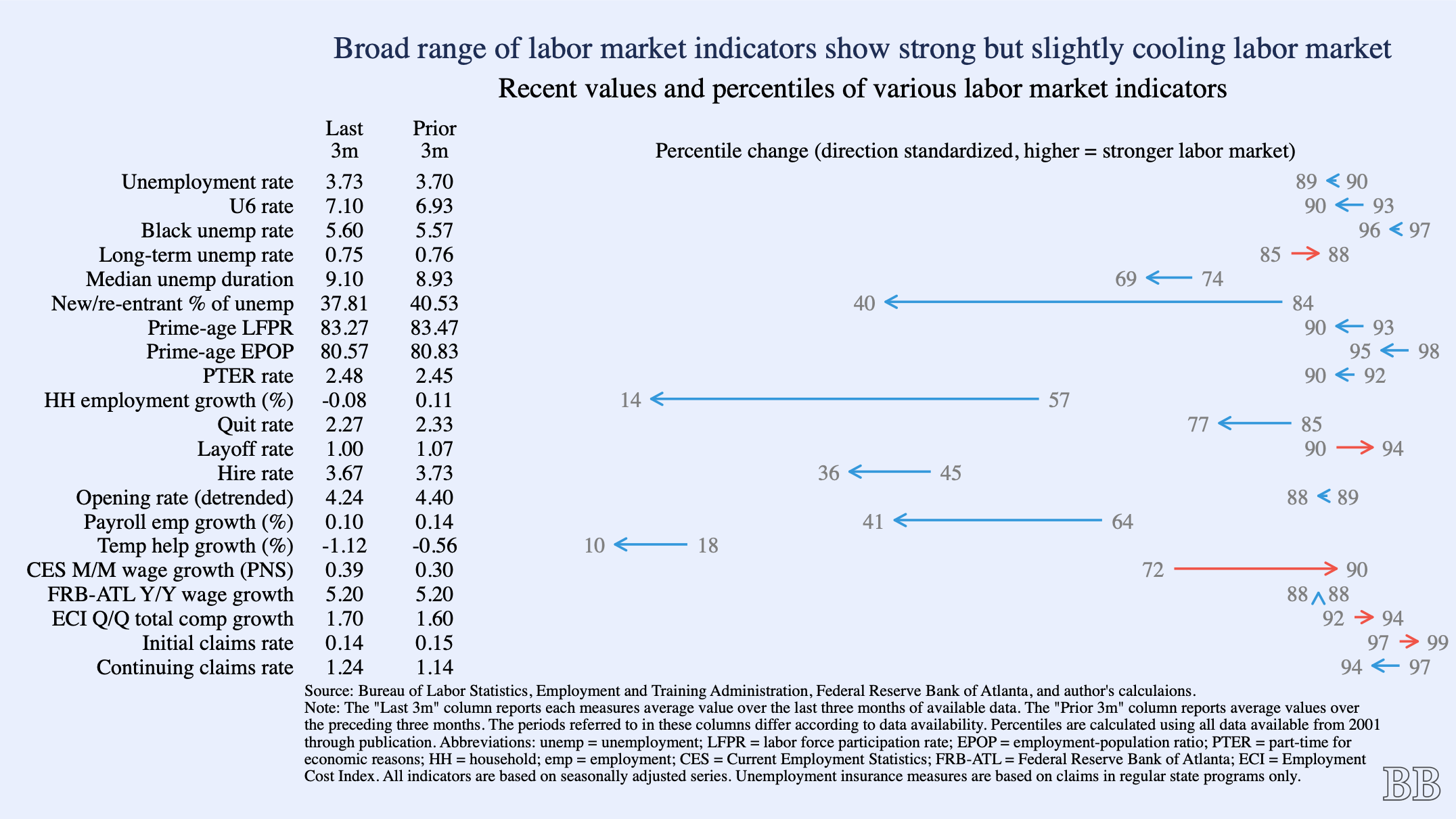

The wide array of available indicators and the uncertainty inherent in any single estimate can make it difficult to assess the labor market using data from a single survey or a snapshot from a single month. Figure 1 compares the average values of indicators covering several dimensions of the labor market over the most recent available three-month period to their values over the preceding three months. The two columns on the left report these values, while the plot on the right shows where the fall in the distribution of each indicator’s values since 2001. Percentile values have been directionally standardized so that higher percentiles correspond with a stronger labor market.1

Of the 21 indicators considered, 14 have current values in the 88th percentile or higher, including several employment, unemployment, and labor force participation indicators. Only two indicators have values in the bottom tercile. On balance, the full set points to a very strong labor market. Indicators related to wage growth and layoffs are particularly strong, and several are stronger over the last three months than over the preceding three. Measures of unemployment and employment levels are also strong and have changed little recently. Measures of employment growth are weaker and have seen more substantial weakening.

The case for optimism: nothing about the current labor market is obviously unsustainable

One might be concerned that the labor market’s strength will be fleeting, a remnant of responses to the pandemic that will dissipate as things return to equilibrium. However, a closer look reveals that the strength of the current labor market is in line with fundamentals, supported by labor market dynamics that are well within historical norms.

Figure 2 plots the relationships between the unemployment rate and several measures of labor market dynamics from the Job Openings and Labor Turnover Survey (JOLTS).2 Panel (a) depicts the Beveridge curve, the relationship between job openings and unemployment, while panel (b) shows a version of that curve constructed using quits, which tend to be high when openings are high.3 In each case, the most recent data, shown in red, show labor market dynamics pretty much where one would expect them to be given the unemployment rate, with openings if anything slightly higher than expected and quits slightly lower. Panel (c) shows that hires are somewhat lower than expected based on the unemployment rate, while layoffs in panel (d) are very much in line with expectations based on historical data. Notably in all four panels, the most recent data points are very close to those observed in 2019 (shown in darker blue).

Figure 3 shows three versions of the wage Phillips curve, depicting the relationship between the unemployment rate and measures of wage growth. The wage measure in panel (a) comes from the Employment Cost Index and is meant to capture quarterly changes in wages within the same types of jobs. It shows notably faster wage growth in the third quarter of 2023 than one might have expected based on pre-pandemic data. The measure in panel (b), the year-over-year change in wages experienced by the median person, also shows faster than expected wage growth. Each of these measures is designed to capture changes in wages experienced within a fixed set of jobs or workers, limiting the influence of changes in the composition of employment or the labor force on measured wage growth. The measure in panel (c), average hourly earnings among all production and non-supervisory workers, is responsive to such changes. It shows monthly wage growth in line with the pre-pandemic experience, and especially in line with that seen in 2019.

Counterintuitively, elevated wage growth could be a problem for sustaining a strong labor market if it generates concerns about (or actual) higher inflation and leads the Federal Reserve to keep monetary policy tighter than it otherwise would have. Labor productivity growth, however, would alleviate this concern. Figure 4 shows the three measures of wage growth considered above alongside a measure of sustainable wage growth that is equal to productivity growth plus the Federal Reserve’s two percent inflation target. From 2001 through 2019, actual wage growth tracked this measure well, and inflation was low and stable. Since the onset of the pandemic, labor productivity has fluctuated widely (partially reflecting shifts in the composition of employment as acutely exposed sectors reacted and adapted to the pandemic), and beginning in early 2022, actual wage growth substantially exceeded the sustainable benchmark. Over the course of 2023, however, productivity has rebounded while wage growth has moderated, bringing actual wage growth closer to a level that would be sustainable.

Wage growth may also have been relatively high over the last two years because workers had more bargaining power than usual in the aftermath of the pandemic. Figure 5 plots the labor leverage ratio, the ratio of quits to layoffs. Higher values reflect greater willingness to quit among workers relative to the likelihood of being laid off, a condition that is more conducive to workers achieving wage gains. This ratio hovered just below 2 before the pandemic. Since then it has risen and fallen alongside wage growth, and it is now approaching its pre-pandemic level. If workers’ bargaining power continues to normalize alongside productivity, any concerns about inflation and potential Federal Reserve responses should moderate. Slower wage growth could also help shore up the weakness in hiring and employment growth discussed above.

Warning sign: employment growth has slowed

Slowing employment growth is the clearest cause for concern in the labor market. The slowdown is evident in the most commonly used measure based on payroll employment, which has averaged 0.1 percent over the last three months, down from 0.14 percent over the preceding three months. While still clearly growing, that rate is good for only the 41st percentile of growth since 2001.4 In the household survey, the prime-age employment-population ratio has also declined over the last few months after hitting its post-Great Recession high.5

Other indicators also suggest that employment growth could slow further in the coming months. The share of unemployed workers who are new entrants or re-entrants into the labor market has declined in recent months, suggesting that workers currently on the sidelines of the labor market are becoming less inclined to get back on the field, so to speak. This shift in the composition of the unemployed often happens around the onset of a recession. Relatedly, as Employ America recently noted, hires of labor force non-participants are also falling. Further, payroll employment in temporary help services, which tends to contract earlier in the business cycle than overall employment, has been trending down since late 2022 and declined by about 1.1 percent each month over the last quarter of 2023.

These indicators, however, come with some caveats. Temporary help services employment has only been measured since 1990, so its tendency to decline earlier than overall employment is based on a sample size of three recessions, the most recent of which had an easily identified cause unrelated to pre-recession labor market dynamics.6 While the composition of the unemployed has a longer track record, the share newly entering or re-entering the labor force is fairly noisy, and its recent values are consistent with those observed since the mid-2010s (outside of the onset of the pandemic).

2019 is ours for the taking

At this point, the labor market side of a “soft landing” doesn’t require anything remarkable or unlikely to happen. While the labor market has certainly cooled relative to its pandemic-era peak, it remains quite strong, and that strength is built on fundamentals that are very much in line with those seen in 2019, a year that saw strong labor market performance without a great deal of concern that it was on the verge of ending. On top of this, business applications boomed early in the pandemic and remain elevated, and these new firms are hiring, adding some dynamism to the labor market.

While wage growth is stronger now than in 2019 and hiring is weaker, normalizing productivity growth should help wage growth return to sustainability, which in turn should make hiring more appealing and help firm up employment growth. With household balance sheets improved, consumer spending continuing to grow, and the Federal Reserve poised to loosen monetary policy by cutting interest rates multiple times this year, labor market performance comparable to 2019 or better should be an attainable and sustainable place to land. Economic expansions don’t die of old age, and at the moment it is difficult to identify another likely cause of death within the labor market.

For example, the unemployment rate tends to have lower values in a stronger labor market, so its percentile values have been inverted (i.e. 3.73 percent unemployment is greater than the unemployment rate observed in only 11 percent of three-month periods since 2001, but it represents a stronger labor market than that observed in 89 percent of those periods) to be comparable to those reported for indicators that tend to have higher values in stronger labor markets, like the employment-population ratio.

Producing this figure using a measure of labor market that is less sensitive to labor force participation decisions, such as the prime-age employment-population ratio, tells a similar story.

Job openings have trended up over time, creating some instability in the relationship with unemployment. The openings series used here has been detrended by regressing the opening rate on a linear trend from the beginning of the series through February 2020, predicting the residuals each month, and adding those residuals to the average value of the opening rate over all available months of data.

The U.S. population has aged substantially since 2001: that year, people at least 65 years old accounted for 12 percent of the population, a figure that had risen to 17 percent by 2022. As the share of the population likely to be interested in working declines, one might expect typical employment growth to decline as well, making more recent months more likely to fall lower in the distribution of monthly employment changes. Of course, this trend has little influence on shifts within the distribution over the last six months.

The less reliable employment growth measure based on the household survey shows a more dramatic slowdown in growth and in fact contraction on average over the last three months.

Temporary help services employment has also been declining since early 2022. Prior recessions began within a few months of this measure beginning to decline. Other pandemic-related labor market shifts may contribute to changes in temporary help services employment.