Beyond the Tax Cuts and Jobs Act: Why It’s Time to Rethink Business Taxation

Corporate integration would make business taxes simpler, fairer, and more efficient

The U.S. tax code has stitched together a patchwork of rules and regulations to tax businesses—a result of more than a century of compromise and incremental change. At its core is a dual tax system for business income that distinguishes between C-corporations, which are subject to double taxation, and pass-through entities, which pass their income to their owners who face a single layer of tax. As a result, businesses that operate similarly in the same markets and industries, and earn the same income, can face very different tax bills depending on their organizational form.

This dual tax system affects the decision-making of businesses and business owners. At the highest level, business owners must balance tax and non-tax factors when choosing how to incorporate. Moreover, once operational, differential tax treatment across business forms affects after-tax returns, diverting resources from their most productive use. Finally, business owners must navigate a tax code that has become increasingly more complex to reconcile tax policies that affect entities and individuals differently. The result is a system that distorts business decisions, encourages tax-driven organizational choices, and undermines fairness.

The expiration of the 2017 Tax Cuts and Jobs Act (TCJA), a tax bill that was largely motivated by the desire for business tax reform, presents an opportunity for policymakers to fundamentally reconsider business taxation. This post outlines how the current dual tax system operates and highlights its inefficiencies. Further, it provides an overview of how standardizing the tax treatment of all businesses under a policy of corporate integration can provide an alternative path forward. By addressing inequities across business forms that persist under the current system, corporate integration presents an opportunity to create a simpler, fairer, and more efficient tax framework.

How is Business Income Earned in the U.S.?

The U.S. tax code maintains a dual system of business taxation that depends on the organizational form of the business. Broadly, a business can be organized in one of four ways: C-corporations, S-corporations, partnerships, or sole proprietorships. From the standpoint of business operations, the organizational form is largely a distinction without a difference. All four types of businesses operate with and compete against each other in nearly every industry and market. For the purposes of determining tax liability, however, this distinction determines whether its earnings will be taxed at the entity level, at the shareholder/owner level, or both.

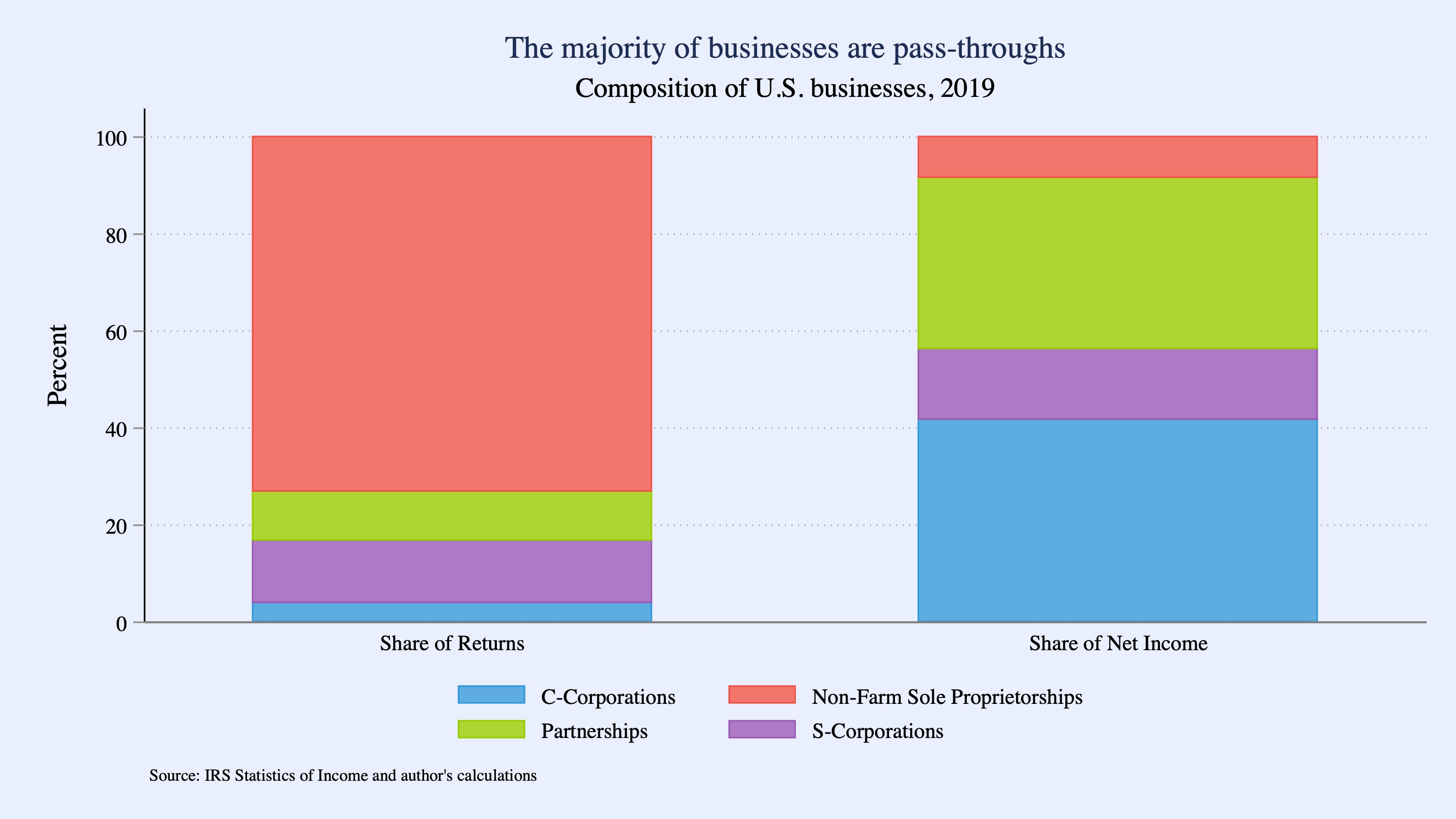

Figure 1 illustrates the distribution of business tax returns and (net) income by organizational form in 2019. Sole proprietorships, which are owned by a single individual or a married couple, constituted a majority of business returns (73%). However, these businesses tend to be small, accounting for only 8% of total business income. In contrast, C-corporations, named after the subchapter of the Internal Revenue Code governing their tax treatment, are typically large entities. Although they represented just 4% of all businesses in 2019, C-corporations earned 42% of total business income. C-corporations are owned by shareholders, with few restrictions on who can hold shares. All publicly traded businesses are required to be structured as C-corporations.

S-corporations, by comparison, are a special type of domestic corporation with stricter ownership rules. They are limited to 100 shareholders, who must be U.S. citizens. S-corporations accounted for 13% of total business returns and 15% of business income. Partnerships, on the other hand, are the most complex business form due to their ownership flexibility. They can have unlimited partners, including individuals, corporations, or even other partnerships, and in some cases, may be traded on public stock exchanges. In 2019, partnerships represented 10% of business returns but earned a significant 35% of business income.

How is Business Income Taxed in the U.S.? - The Dual System of Business Taxation

Entity-Level Corporate Tax

Taxable income that is earned by C-corporations faces two layers of taxation. First, corporate income is taxed at the entity level in the year it is earned, according to the corporate income tax schedule. The 2017 Tax Cuts and Jobs Act permanently reduced the corporate income tax rate from a graduated marginal schedule with the top rate of 35% to a flat tax schedule with a rate of 21%. In a simplified sense, a C-corporation that earns $1,000,000 in taxable income this year faces a $210,000 corporate income tax bill, abstracting away from tax preferences like specialized deductions and tax credits.

After paying the corporate income tax, the C-corporation must decide what to do with its after-tax earnings of $790,000: distribute some or all to its shareholders as a dividend, retain some or all inside of the business for future use, or some combination of these two behaviors.1 When after-tax earnings are distributed to shareholders as a dividend, this income is taxed at the individual level. This is the second layer of tax for C-corporate earnings.

Suppose, for example, that the C-corporation immediately distributed all its after-tax earnings to its shareholders. Qualified dividends, which characterize most equities returns for U.S. shareholders, are taxed at a top preferential rate of 20%. In this case, the shareholders would collectively owe an additional $158,000 in dividend income tax. This brings the total tax bill on $1,000,000 in corporate taxable income to $368,000: $210,000 in corporate income tax and $158,000 in dividend tax. In other words, corporate owners face a total tax rate of 36.8% in this illustrative example, earning just $632,000 in after-tax earnings for every $1,000,000 in taxable income.

Although C-corporations face a 21% statutory corporate tax rate, they can also benefit from one or more tax preferences in a way that reduces the share of earnings that they pay in corporate income tax. For example, certain business activity, such as investment in low-income housing developments, expenses associated with research and experimentation, clean energy investments, generates tax credits that can be used to reduce tax liability. Additionally, certain businesses may be eligible for tax deductions that further reduce their taxable income. For example, small businesses can accelerate the rate at which they deduct the cost of their capital investments. The effective tax rate (ETR), or the ratio of tax payments to profits, reflects these tax preferences; the ETR is, therefore, typically smaller than the statutory tax rate at each layer of tax.2 Effective tax rates can vary substantially across C-corporations and over time. Pomerleau (2024) estimates that the average effective tax rate (AETR) for C-corporate income across both layers of tax was 29.3% in 2024.

Individual-Level Pass-Through Tax

Pass-through businesses, which include S-corporations, sole proprietorships, and certain partnerships, do not face an entity-level tax. Instead, the taxable income of pass-through businesses is “passed through” to their owners and is taxed like wage and other employment income, facing the individual income tax.3 The individual income tax schedule is a graduated tax schedule with rates that begin at 10% and increase to the top rate of 37%.

For illustrative purposes, consider a pass-through business with a single owner that earns $1,000,000 in taxable income. If all of the owner’s pass-through income were to face the top marginal tax rate, then the owner would owe an additional $370,000 in individual income tax.4 Notice that this tax bill ($370,000) is roughly similar to the total tax liability for $1,000,000 in C-corporate income previously described ($368,000). In other words, the total tax across the two-layers faced by C-corporate income can be similar to the single tax faced by pass-through business owners. However, this is, in many ways, a best-case scenario.

Tax Disparities by Business Form

The twin-system for business tax creates disparities in the tax faced by otherwise similarly situated businesses.

To begin, the same pass-through business can be subject to a wide range of tax rates depending on the tax position of each owner, as determined by the graduated individual income tax schedule. To see this, consider again the same pass-through business that earned $1,000,000 in taxable income, but now suppose instead that the pass-through is owned by 100 owners instead of one owner, and that each owner’s share of taxable income is $10,000.

Each owner’s tax bill depends on their individual tax position, including any other taxable income that they may have earned. Assume that each owner earns enough additional income to place them in the middle of the 22% tax bracket.5 In this case, each owner would face a 22% marginal tax rate on their share pass-through business income ($2,200). Across all 100 owners, the total tax $1,000,000 in pass-through income would be $220,000. Recall that the same pass-through business with a single owner who earned enough income to face the top marginal tax rate of 37% owed $370,000 on the same pass-through income.

Moreover, the TCJA introduced a special deduction, known as the Section 199A deduction, to provide additional tax relief to pass-through business owners on top of the reduction in individual tax rates. The maximum value of this deduction is 20% of pass-through business income. For illustrative purposes, suppose the previously described single-owner pass-through qualified for the full value of the 199A deduction. In this case, the owner would benefit from a $200,000 deduction on $1,000,000 in pass-through income. If this income were subject to the top marginal tax rate—the worst-case scenario from the standpoint of calculating tax liability—then the owner would face a tax bill of $296,000 on this pass-through business income. In this example, the 199A deduction reduced the total tax on $1,000,000 in pass-through income from $370,000 to $296,000. The 199A deduction is infamously more complicated than this, but at a high level, this simplified calculation demonstrates how the 199A deduction reinforces disparities in the tax treatment of pass-through business income compared to C-corporate income.

Pomerleau (2024) estimates that, ignoring the 199A deduction, the AETR on pass-through business income was 29.5% in 2024—similar to the AETR on C-corporations (29.3%). However, taking in 199A into account, Pomerleau finds that the AETR on pass-through businesses was 23.7%, more than 5 percentage points below the AETR on C-corporations.

The AETR captures the overall tax burden on all business income, including from both old and new investments. In contrast, economists and policymakers typically focus on the marginal effective tax rate (METR), which measures the tax burden in income generated from new investment. The METR is calculated by estimating the additional tax on $1 in business income generated by a new investment. It reflects the tax system’s impact on projects that just break-even in present value, summarizing the extent to which taxes distort investment decisions.

Reducing the METR—for example, through a reduction in the business tax rate—encourages investment by lowering the return required for a project to break even. Disparities in the METR across business forms distort the allocation of investment, potentially shifting capital inefficiently across firms.6 To this end, Pomerleau (2024) finds that the METR on C-corporate income was 22.1% in 2024, exceeding the METR on pass-through income by more than four percentage points (17.7%).

How Did We Get Here? A Brief History of US Business Taxation

The modern corporate income tax was first introduced in 1909 as a 1% tax on businesses with more than $5,000 in taxable income. At this time, the corporate income faced only a single layer of taxation because the federal government did not have the authority to levy an income tax. In 1913, the 16th amended extended the authority to impose federal individual income taxes, effectively creating the double tax on corporate income. Once individuals began paying taxes on their dividend income, the system of double taxation for corporate profits became institutionalized, with corporations paying taxes on their profits and shareholders paying taxes on distributions. Between 1913 and 1958, the top marginal corporate income tax rate rose from 1% to 52%.

In contrast, sole proprietorships—one of the oldest and simplest forms of business organization—have always been taxed differently. Before the ratification of the 16th amendment, sole proprietors were not subject to federal income tax because the government lacked the authority to tax individual income. After the amendment, sole proprietorships became an example of pass-through taxation, as they were allowed to report business income and expenses directly on their personal tax returns. These businesses require minimal legal formalities compared to other types of businesses, so they have long been a popular choice for new and small businesses.

S-corporations were created by Congress in 1958 to formalize the concept of a pass-through business. Specifically, the Small Business Tax Act of 1958 established S-corporations as a legal business form under Subchapter S of the Internal Revenue code, allowing businesses to benefit from limited liability while avoiding the double tax on business income. Instead, profits are passed directly to shareholders and taxed at individual income tax rates. Over time, additional pass-through business forms have been introduced, including various types of partnerships—domestic general partnerships, domestic limited partnerships, domestic limited liability partnerships, and foreign partnerships—each offering flexible ownership structures and pass-through tax treatment.

The emergence and growth of pass-through entities has transformed the landscape of U.S. business taxation. Figure 2 depicts the share of businesses by organizational form, excluding non-farm sole proprietorships, from 1980 – 2015. In 1980, C-corporations represented 53% of all formal businesses. A series of tax reforms between 1981 and 1986 dramatically altered the tax advantage of organizing as a pass-through by cutting the top individual income tax rate from 70% in 1980 to 28% in 1988; by comparison, the top corporate tax rate fell from 46% to 34%. Most experts attribute the subsequent rise in pass-through businesses to these tax changes. Finally, the TCJA introduced historic reductions to business tax rates. As previously described, these changes collectively served to maintain the tax advantage enjoyed by pass-through business income relative to C-corporate income that was present prior to the TCJA while reducing the overall business tax burden on investment.

What is the Problem with the Current Approach?

The disparate tax treatment of C-corporate and pass-through income distorts business decision-making. At the highest level, the choice of business form is driven by the desire to maximize after-tax profit. While non-tax considerations play a role—for example, access to capital and liability protection—differences in tax treatment can inefficiently push businesses and capital into one form over another. Key tax factors driving this distortion include the handling of business losses, the tax advantages of debt financing, variations in incentives for investment, and the availability of targeted deductions. These differences can be seen by comparing the METRs across business forms. As previously described, Pomerleau (2024) shows that METRs are lower for pass-through businesses than C-corporations, making the pass-through form more attractive. Unfortunately, there is limited quantitative evidence that speaks to the magnitude of this distortion (de Mooj and Ederveen, 2008).

Maintaining the dual business tax system has also increased the complexity of the tax code. While tax policies can be designed to address business concerns broadly, applying them across both entity-level and individual tax systems necessitates complicated regulations. For instance, tax credits targeting small businesses are typically based on entity-level criteria, like total assets, employment, or income. However, for pass-through businesses, additional rules are required to allocate these measures across owners or determine eligibility, adding layers of complexity.

Finally, the differences in the tax treatment of C-corporate and pass-through income raises concerns about the progressivity of the tax code. Pass-through income tends to be more concentrated among high income owners than corporate equity. For example, the Joint Committee on Taxation (JCT) estimated that in 2019, the bottom 50 percent of the income distribution earned 4% of their income from corporate sources and 9% of their income from pass-through businesses. For those in the 90th to 95th percentile, these shares rose to 7% and 12%, respectively. At the very top, individuals in the top 0.1% earned 35% of their income from corporate sources and 28% from pass-throughs. This means that higher income households not only disproportionately benefit from greater after-tax returns, but that they also benefit from certain provisions that are targeted to pass-through businesses, like the TCJA’s Section 199A deduction.

How Can Business Taxation be Fundamentally Reformed?

For over a decade, policymakers have recognized the need for fundamental business tax reform.

For example, President Obama’s White House, together with the Treasury Department, released The Presidents Framework for Fundamental Business Tax Reform in 2016, which called for business tax reforms that reduced complexity, enhanced the competitiveness of U.S. businesses, and encouraged job creation and investment. At the same time, the Republican House of Representatives released its own blueprint for fundamental business tax reform, A Better Way, which advocated for replacing the corporate income tax with a corporate cash flow tax. Like the 2017 TCJA, each of these efforts offered differing approaches to reforming the corporate tax system. However, they all retained the unequal tax treatment of pass-through and corporate income.

A more comprehensive approach to business tax reform lies in corporate integration. This policy seeks to eliminate the disparities between corporate and pass-through tax treatment by creating a unified system that taxes all business income once, regardless of organizational form. Unlike the more complicated policies and proposals of the last decade, integration offers an opportunity to simplify the tax code, enhance fairness, and reduce distortions that affect business decisions.

Pomerleau (2024) explores three distinct proposals for business integration, including an analysis of the trade-offs associated with each option. The first proposal, a comprehensive business income tax (CBIT), would introduce a single entity-level tax that applies to all businesses, with additional adjustments made to the tax base to exclude dividends from taxation at the individual level. Under this system, individual income tax would exclude business income, such as dividends and capital gains from corporate equities. Similar policies have been proposed over the last several decades, including by U.S. Treasury Department (1992) and in the well-known X-tax model (Carroll and Viard, 2012). The CBIT is also resembles Estonia’s business tax system.

The second proposal, a shareholder allocation model or “flow-through” model, would tax all income at the individual level, similar to current pass-through tax treatment. Businesses would determine their taxable income at the entity-level and pay a withholding tax at the corporate income tax rate. Profit, whether distributed or not, would then be allocated to shareholders and taxed according to individual marginal tax schedules. US shareholders would receive a tax credit for the withholding tax on their share of allocated profits.

The third proposal, a credit imputation model, retains the blended tax approach taken by the current system. Under the credit imputation model, C-corporations would continue to pay an entity-level tax, but shareholders would receive an imputation credit equal to the taxes paid at the corporate level. When profits are distributed to the shareholders, shareholders would also receive their share of the imputation credit. Individuals’ income tax rates would stay the same, but dividends from C-corporations would be taxed like ordinary income instead of receiving preferential rates. Like the flow-through model, the imputation credit would only be made available to US shareholders, retaining the double tax on foreign equity holders. This approach is comparable to Australia’s tax system and aligns closely with a policy proposed by Eric Toder and Alan Viard (2016).

As discussed by Pomerleau (2024), each of these three proposals reduce inefficiencies and offer simplifications relative to the current system. All proposals, for example, would reduce the difference in the METR between corporate and pass-through income, reducing the distortion to capital allocation. However, each proposal introduces trade-offs. For example, while the CBIT is likely to be the simplest to implement and eliminates differential tax treatment, it likely requires high marginal tax rates on business income. In this way, the CBIT may affect the competitiveness of US businesses and the attractiveness of the US as a location for multinationals. The shareholder allocation model makes some progress in reducing the difference in METRs across business forms, but it does so by maintaining much of the same complexity as the current system. Finally, the credit imputation proposal would be the easiest to implement because its design is congruous with the current status quo for US businesses, but it makes the least progress in reducing differences in METRs.

Conclusion

There is no simple solution that resolves the disparity in tax treatment across business forms in the United States. The double taxation of corporate income has been a feature of the tax system since 1913, while the pass-through business form has served as a tax-reducing strategy since its introduction in the 1950s. Over time, this two-tracked system for taxing business income has resulted in complexity and inefficiency, distorting business decisions and undermining the tax code’s fairness.

The 2025 expiration of the TCJA presents an opportunity for policymakers to rethink the structure of business taxation. Integration offers a pathway to a simpler, fairer, and more efficient tax system that better supports economic growth and innovation by minimizing differences in tax burdens for similarly situated businesses and investments. However, much of the current policy discussion has centered on which of the TCJA’s $5 trillion of expiring provisions to extend—many of which reinforce the tax advantages of pass-through businesses over C-corporations.

Instead of maintaining these tax advantages, Congress should prioritize reforms that align with the principles of integration to create a more balanced and growth-oriented tax system.

This is, of course, a simplification for illustrative purposes. C-corporations can also use after-tax earnings, for example, to buy back shares.

Note that the ETR can vary depending on the measure of profit used in the denominator. Generally, researchers take care to study a measure of profit that is not affected by tax laws themselves. A common measure available for large firms in the tax data is pretax book income, reported on Schedule M-3.

Pass-through businesses must fully distribute taxable income to their owners, regardless of whether some share of taxable income is retained by the business.

This, again, is an illustrative calculation. For example, I abstract away from whether some or all of the economic profit is distributed as wage income—a choice faced by pass-through business owners with follow-on tax implications. Under these assumptions, suppose, for example that the owner was a single filer with taxable income from other sources in excess of $609,351, the threshold for the top marginal tax rate. In this case, the pass-through business income can be thought of as being taxed exclusively at the top individual marginal tax rate of 37%.

In 2024, the 22% tax bracket for single-filers was $47,151 - $100,525 and $94,301 to $201,050 fo joint-filers.

Empirical evidence on the extent of this distortion is limited, partly due to the significant data requirements needed to address this question. For instance, observing the marginal tax rate—or even estimating the likely marginal tax rate—faced by owners of pass-through businesses is best estimated with restricted-access tax data. Researchers at the US Treasury Dept found that the tax changes implemented in the 1980s increased the likelihood of organizing as a pass-through.

| A guest post by

|

The administrative complexity of C and non C incorporation and that non-C income can be “taxed twice” is inconsequential and downstream from taxing business income. Business income is income of the owners of the business. That is where it should be taxed. All business income should be passed through to owners. This would also be more compatible with conversion of the personal _income_ tax into a personal _consumption_ tax.

“The expiration of the 2017 Tax Cuts and Jobs Act (TCJA), a tax bill that was largely motivated by the desire for business tax reform …”

If business tax reform were the main reason for the "Tax Cuts for the Rich and Deficits Act of 2017" :), they could have reduced rates more and made up the revenue loss with increase in personal income tax rates. Instead, they also reduced personal collection (except for limiting SALT deductions), adding to the huge growth-devouring deficit.

I'm "liking" this for raising the issue even before reading whether I agree or not!